Introduction

As you make the critical decision to save for your retirement, it’s essential to understand the different types of funds/schemes that are in the retirement benefits sector. This understanding is to ensure that you are saving for your retirement in a scheme that best fits your goals.

Despite the vital role that the retirement benefits sector plays in our lives, most people don’t understand how retirement benefits scheme work and their features. We aim to change that so do read on.

There are several ways to classify retirement benefits schemes:

Based on payment of your benefits at retirement, a scheme can either be a provident fund or a pension fund.

Based on the type of membership, a scheme can be an individual scheme or an occupational scheme.

Based on the mode of investment, a scheme can either be guaranteed fund or segregated fund.

In this article, we will shed more light on the differences between a guaranteed fund and a segregated funds, and the features one should consider before choosing between the two.

Guaranteed Funds are offered by insurance companies where the members’ contributions are invested as a pool of fund. The insurance company then guarantees a minimum rate of return. Should the actual return surpass the minimum guaranteed rate, the insurance company tops up the minimum rate with a bonus rate of return.

Segregated Funds are those where members’ contributions are invested directly by the Trustees through an appointed Fund Manager. The Trustees establish an appropriate Investment Policy Statement (IPS) which is then implemented by the Fund Manager. The scheme directly holds the investments and the returns are fully accrued to the fund for the benefit of members.

Comparison between Guaranteed Funds and Segregated Funds.

Rate of Return

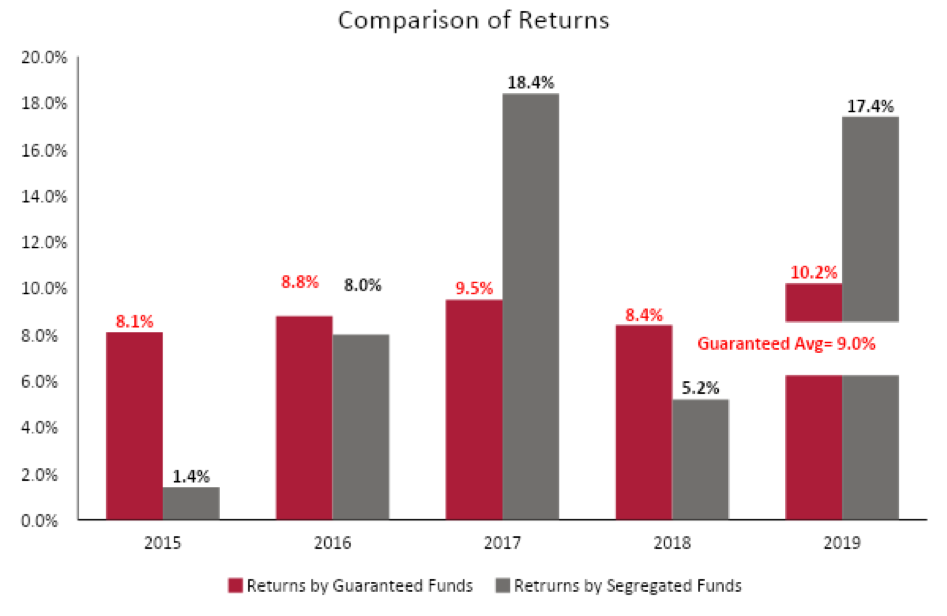

Historically, segregated funds have offered higher returns compared to guaranteed funds. Guaranteed funds are mostly invested in government securities, which offer lower returns compared to segregated funds. Segregated funds have a more balanced portfolio, ensuring members benefit from the high-risk, high-return.

Looking at the last five years to December 2019, guaranteed funds have offered an average return of 9.0%, compared to the average return of 10.1% offered by segregated schemes. In addition to the conservative investment by guaranteed funds, insurance companies also hold some reserve every year to cater for years where the market’s.

performance is below the promised rate. In contrast, in segregated funds, all returns are accrued to the member.

Level of Risk

Guaranteed funds are less risky as they ensure capital preservation of members’ benefits as well as offering a minimum guaranteed rate of returns. They are therefore attractive to members with a conservative risk appetite. Segregated funds, on the other hand, are subject to market performance, and this entails higher risk than guaranteed funds.

Governance

In a guaranteed fund, less management is required as the funds are invested by the insurance company, which also sets the minimum guaranteed rate. On the flip side, segregated funds require much more staunch governance as a trustee oversees the investments of the funds through the investments policy statement (IPS), and they can revise the IPS to cater for the changing needs of the fund.

A Guaranteed Fund or a Segregated Fund? What’s right for you?

Age

Guaranteed funds are more attractive to people who are close to retirement as they cannot afford to take up high risk with their investment. On the other hand, segregated funds are suitable for the younger member who have a longer horizon to retirement as they can take up the risk that comes with segregated funds and have time to recover in the event of poor market performance. This then allows them to enjoy the attractive returns offered by segregated funds.

Rate of Return

As discussed, a member who has a capacity for higher risk and hence higher returns should invest in a segregated fund. In contrast, those with lower capacity for risk, and are comfortable with the lower rate of returns but with capital preservation, should join guaranteed funds.

Conclusion

In addition to the above pointers, it’s crucial to engage a financial advisor for more guidance on choosing the scheme that best serves your need.

You can get in touch with a Genghis Capital financial advisor by writing to info@genghis-capital.com.